What Is Series A Funding Series A funding is the first significant round of institutional venture capital financing a startup raises after demonstrating early traction through seed funding. It typically involves selling preferred stock to professional VC firms in exchange for $5M–$30M in capital, at a pre-money valuation generally ranging from $15M to $80M. Unlike seed rounds, Series A is a priced round — meaning investors receive a formal equity stake based on an agreed company valuation. Startups pursue Series A funding to scale their go-to-market engine, expand the team, and achieve the KPIs necessary to prepare for a Series B round.

Series A Funding Meaning :

Why Series A exists — and what it signals :

When a startup graduates from seed funding, it has (usually) answered the hardest early question: Does anyone want this? Series A financing exists to answer the next question: Can we build a repeatable, scalable machine to serve that demand?

Series A is the bridge between early validation and real-scale growth. Investors at this stage are not betting on an idea — they are betting on a team with a proven product, early revenue signals, and a credible plan to 10× the business. In exchange for that capital, founders issue preferred stock — shares with downside protections like liquidation preferences and anti-dilution provisions — which differs structurally from the common stock held by founders and employees.

The U.S. Securities and Exchange Commission (SEC) regulates these securities offerings. Most Series A rounds are structured as private placements under Regulation D, sold exclusively to accredited investors. The National Venture Capital Association (NVCA) publishes model legal documents that standardize much of the term sheet and investor rights language used in these rounds.

According to Carta’s Q4 2024 State of Private Markets report, the median pre-money valuation at Series A was $45 million — up 14% year-over-year — with median deal sizes historically ranging from $10M to $15M and average raises closer to $22M.

Series A vs Seed vs Series B vs Series C :

Each funding round has a distinct purpose, investor type, and proof requirement. Below is the definitive comparison.

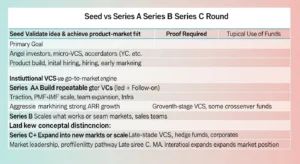

Table 1: Seed vs Series A vs Series B vs Series C :

| Round | Primary Goal | Typical Investors | Proof Required | Typical Use of Funds |

| Seed | Validate idea & achieve product-market fit | Angel investors, micro-VCs, accelerators (YC, etc.) | Prototype, early users, founding team | Product build, initial hiring, early marketing |

| Series A | Build repeatable go-to-market engine | Institutional VCs (lead + follow-on) | Traction, PMF signals, unit economics | Sales/marketing scale, team expansion, infra |

| Series B | Scale what works aggressively | Growth-stage VCs, some crossover funds | Proven revenue model, strong ARR growth | Aggressive hiring, new markets, sales teams |

| Series C+ | Expand into new markets or prep for exit | Late-stage VCs, PE, hedge funds, corporates | Market leadership, profitability pathway | M&A, international expansion, pre-IPO prep |

The key conceptual distinction: Seed funding discovers whether your thesis is correct. Series A executes that thesis at scale. Series B accelerates execution. Series C defends and expands market position.

Typical Check Size, Valuation, and Dilution Ranges :

These are ranges, not guarantees — market conditions, sector, and geography all matter.

- Check size: $5M–$30M (median ~$12M–$15M in the U.S.; average ~$22M in 2024)

- Pre-money valuation: $15M–$80M (median ~$45M in Q4 2024 per Carta)

- Investor dilution: Typically 15%–25% of the company per round

- Option pool refresh: Investors commonly require a 10%–20% option pool pre-money, meaning it dilutes existing shareholders (primarily founders) before the new investment is calculated

Understanding pre-money vs post-money valuation is critical here. If your pre-money valuation is $40M and investors put in $10M, the post-money valuation is $50M — and the investors own 20% of the company. This directly impacts your cap table and every subsequent round’s dilution math.

What “Lead Investor” Means and Why It Matters :

In any Series A, one VC firm acts as the lead investor. They negotiate the term sheet, set the valuation, and typically take a board seat. Everyone else in the round (follow-on investors) participates on the terms the lead has already negotiated.

Choosing the right lead is one of the highest-leverage decisions a founder makes. Firms like Sequoia Capital and Google Ventures (GV) are examples of institutional investors who regularly lead Series A rounds — bringing not just capital but partner networks, hiring pipelines, and operational playbooks. A weak or misaligned lead can poison a cap table and complicate every future raise.

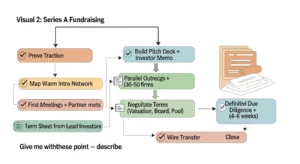

How Does a Series A Round Work ?

A typical Series A process takes 3–6 months from first outreach to wire. Here’s the step-by-step sequence.

Step 1 — Prove Traction (What Metrics Matter by Business Model)

Before you pitch a single investor, your metrics need to tell the story. VCs will pattern-match against benchmarks in their portfolio.

What to show by business model:

- SaaS / subscription: $1M–$3M ARR, 2–4× YoY growth, net revenue retention (NRR) >100%, monthly churn <2%, LTV:CAC ratio ≥3:1

- Marketplace: Strong GMV growth, healthy take rate, supply/demand liquidity on both sides

- Consumer app: DAU/MAU >40%, strong D30/D60 retention curves, organic growth > paid

- Deep tech / hardware: Letters of intent, pilot contracts, clear IP moat

The NFX fundraising framework identifies 6+ months of consistent month-over-month growth — ideally 10%+ MoM — as a core signal that separates noise from a real growth engine.If you can’t show durability, you’ll struggle to close.

Step 2 — Build the Fundraising Narrative (Deck + Memo)

Your pitch deck is not a product demo — it’s a business thesis. The best Series A decks follow a tight narrative arc:

- The problem — specific, large, underserved

- Your solution — and why now (what changed in the market?)

- Traction — the evidence that your solution works

- Business model — how you capture value

- Market size — TAM/SAM/SOM (be realistic, not delusional)

- Go-to-market — your customer acquisition engine

- Unit economics — CAC, LTV, payback period, burn rate

- Team — why you win this market

- The ask — amount, use of funds, milestones it unlocks

Some founders also write a 2–3 page investor memo alongside the deck for VCs who prefer deep reading. The YC Startup Library has excellent free templates for both formats.

Step 3 — Investor Targeting + Warm Intros :

Cold outreach to VCs converts at under 1%. Warm introductions from portfolio founders, angels, or mutual connections convert dramatically higher. Invest serious time in mapping your intro network before you send a single email.

Targeting criteria:

- Check size alignment (don’t pitch a $500M growth fund for your $8M Series A)

- Sector thesis match (some VCs only do fintech, others only SaaS, etc.)

- Stage focus (many VCs have “sweet spots” — don’t pitch a seed fund for a Series A)

- Portfolio conflicts (they won’t back your competitor)

- Partner-level interest, not just associate-level

Build a 30–50 firm target list. Rank by tier. Run parallel processes — never sequential — to create genuine momentum. Per NFX, building VC relationships 6+ months before you formally raise dramatically improves outcomes .

Step 4 — Diligence + Term Sheet Basics :

Once a lead VC decides they want to invest, they issue a term sheet — a non-binding document outlining the key economic and governance terms of the deal.

The most consequential terms:

- Pre-money valuation — directly determines your dilution

- Liquidation preference — how investors get paid in an exit (1× non-participating is standard; 2× or participating preferred is founder-hostile)

- Anti-dilution provisions — broad-based weighted average is standard; full ratchet is not

- Board composition — who controls the board post-round?

- Pro-rata rights — can existing investors maintain their % in future rounds?

- Option pool — size and timing relative to pre-money valuation

After term sheet signing, the lead VC runs formal due diligence — typically 2–6 weeks of financial, legal, technical, and reference checks. Refer to our due diligence checklist →. NVCA publishes model legal documents that are widely used as a baseline for negotiations.

Step 5 — Close + Post-Close Governance :

Closing involves lawyers drafting definitive documents (Stock Purchase Agreement, Investor Rights Agreement, Co-Sale/ROFO Agreement, Voting Agreement), signatures, and wire transfer. Total closing timeline post-term-sheet: typically 4–8 weeks.

Post-close, the biggest structural changes are:

- Board seat added — your lead investor now has governance rights and fiduciary duties

- Reporting cadence established — monthly or quarterly financial packages, KPI dashboards, board updates

- Milestones agreed — what must you hit before the next raise? Define them clearly with your board from day one

What Do Series A Investors Look For?

Product-Market Fit Signals :

Product-market fit (PMF) is not a feeling — it’s a measurable state. Series A investors want to see:

- Cohort retention: Do users/customers come back? D30 retention >30% (consumer), net revenue retention >100% (B2B SaaS)

- Organic growth: Is word-of-mouth a meaningful channel? NPS scores above 50 are a strong signal

- Pull vs push: Are customers seeking you out, or are you pushing hard to acquire each one?

- Reduction in churn over time: Early cohorts should churn less as you improve the product

Go-to-Market Clarity and Unit Economics :

Even with strong PMF, investors won’t back a company with a broken go-to-market. They need to see:

- CAC payback period: Under 12 months for SaaS is healthy; under 6 months is excellent

- LTV:CAC ratio: ≥3:1 is the baseline; ≥5:1 is compelling

- Burn rate and runway: Ideally 18+ months of runway at close; burn multiple (net burn / net new ARR) below 1.5×

- Channel attribution: Know which channels work and why — and show proof you can scale them

A vague go-to-market plan is the #1 reason Series A-ready companies fail to close their rounds.

Team, Hiring Plan, and Execution Risk :

At Series A, VCs are buying the team as much as the traction. The questions they’re quietly asking:

- Can this founding team attract A-players?

- Do they have the operational discipline to deploy $10M–$20M without losing control?

- Are there dangerous single points of failure (e.g., only the CEO can close enterprise deals)?

- Does the hiring plan make sense given the use of funds?

Come with a clear 18-month hiring roadmap — broken out by function, timing, and cost — that directly ties to your post-Series A growth plan.

When Should a Startup Raise Series A ?

There’s no universal trigger, but the strongest Series A fundraises happen when you have more demand than your current capital can serve — not when you’re running out of money.

A practical readiness framework:

- You’ve hit $1M–$3M ARR (SaaS) or equivalent traction in your model

- MoM growth has been consistent for 6+ months

- You know your CAC, LTV, and payback period with real data

- You have 6–9 months of runway — enough to run a proper process

- Your founding team has identified key hires capital would unlock

- You’ve spoken informally to 3–5 investors who’ve indicated interest

“Too Early vs Too Late” Warning Signs :

Signs you’re raising too early :

- ARR below $500K with no clear path to $1M+

- Churn above 5% monthly

- No consistent growth trend — still experimenting with product

- Investors are pointing you to seed funds, not writing checks

Signs you’re raising too late :

- Under 3 months of runway — you’re negotiating from desperation, and investors can smell it

- Growth has plateaued without capital infusion

- Competitors have already raised Series A and are pulling ahead

- Key hires have left because equity upside feels uncertain

The sweet spot: raise when you’re at an inflection point with strong momentum, ample runway to run a process, and clear capital deployment thesis.

How to Prepare for Series A Funding :

Preparation should start 6–12 months before you plan to formally raise. Here are the two most critical preparation tracks.

Data Room Checklist (Documents to Prepare)

A well-organized data room can cut 1–2 weeks off your closing timeline, according to YC’s General Counsel Jason Kwon.

Table 2: Series A Readiness Checklist :

| Metric / Asset | Why It Matters | How to Show It |

| MRR / ARR with growth chart | Primary traction signal | Monthly revenue waterfall by cohort |

| Net Revenue Retention (NRR) | Proves customers expand, not just survive | Cohort expansion/contraction table |

| CAC by channel | Validates scalability of acquisition | Channel-level cost attribution report |

| LTV model | Shows long-term unit economics | Revenue per cohort × average life |

| Burn rate + runway | Risk management signal | 13-week cash flow model + bank statements |

| Cap table (fully diluted) | Investors need to see ownership structure | Up-to-date cap table via Carta or Pulley |

| Corporate records | Legal due diligence baseline | Certificate of Incorporation, bylaws, board minutes |

| IP assignments | Protects investor position | Employee IP agreements, patent filings |

| Material contracts | Surfaces risk, shows traction | Top 10 customer contracts, key vendor agreements |

| 3-year financial model | Shows capital deployment logic | Revenue, COGS, headcount, burn projections |

| Org chart + hiring plan | Validates team execution capacity | Current team + 18-month role roadmap |

| Customer references | Third-party validation of PMF | 3–5 referenceable customers ready to speak |

Core data room folders to build :

- /Corporate — Articles of incorporation, bylaws, board consents, stockholder agreements

- /Financials — Historical P&L, balance sheet, cash flow, cap table, financial model

- /Legal — IP assignments, material contracts, employment agreements, SAFE notes, prior term sheets

- /Product — Product roadmap, technical architecture overview

- /Sales & Marketing — Pipeline, CRM export, cohort data, channel attribution

- /People — Org chart, offer letters, equity schedule, employee handbook

Cap Table + Option Pool Planning :

Before you raise, clean your cap table. Messy SAFEs, unconverted notes, or undocumented equity promises will slow diligence and spook investors.

Key pre-Series A cap table actions:

- Convert outstanding SAFEs and convertible notes — understand their dilutive impact at various valuations

- Refresh your option pool — investors will typically require a 10%–20% option pool on a post-money basis, which is actually carved out pre-money (i.e., it dilutes founders before the round price is set). For example, a 15% post-money option pool on a $45M pre-money valuation means approximately ~7.5M worth of shares added pre-investment — all coming from existing shareholder dilution

- Complete pending equity grants — as YC’s diligence checklist notes, once a term sheet is signed, a material event may have occurred that invalidates your current 409A valuation, forcing higher strike prices on new grants.

- Model post-close dilution — run scenarios at $30M, $45M, and $60M pre-money to understand founder and employee ownership at each outcome

For a deep dive, see our guide to startup valuation methods.

Common Series A Mistakes (and How to Avoid Them)

Avoid these eight pitfalls — each one has derailed otherwise fundable rounds.

- Pitching without a long-term funding narrative. Investors ask: “What’s the Series B story?” If you can’t answer, they’ll question whether you’ve thought through the business. Map your path from Series A → B → C before your first pitch meeting.

- Taking the first term sheet out of desperation. Bad terms compound across every future round. A 2× participating preferred liquidation preference from your Series A investor can devastate founder returns at acquisition. Evaluate every term — not just the headline valuation.

- Targeting the wrong investors. Approaching a $1B growth fund with an $8M ask wastes everyone’s time. Targeting a fintech specialist VC with a healthcare product is equally wasteful. Research partner thesis, check size, and portfolio conflicts before you request an intro.

- Not justifying the amount you’re raising. “We’re raising $12M” means nothing without “…to hire 8 engineers, fund 18 months of marketing, and reach $4M ARR — which unlocks our Series B at 3× the current valuation.” Tie every dollar to a milestone.

- Underestimating funding needs. Aiming for only 12 months of runway is dangerous. Fundraising is distracting; targeting 18–24 months of burn gives you time to execute without the pressure of re-entering the market too soon.

- Lacking a clear go-to-market narrative. If you can’t articulate your customer acquisition engine — cost, channel, conversion rate, and scalability — investors will pass. This is not a product problem; it’s an execution risk red flag.

- Ignoring macroeconomic context. A $60M pre-money valuation your competitor achieved in 2021 may be completely irrelevant in 2025. Calibrate your valuation expectations to current market data, not peak-cycle comps.

- Overcomplicating the pitch deck. More slides ≠ more conviction. A crisp 12–15 slide deck that tells a clear story beats a 40-slide technical deep-dive every time. Your audience is a generalist investor, not a peer engineer.

How GoCloud Helps Startups Prepare for Funding :

In addition to helping startups build scalable cloud infrastructure, GoCloud also supports founders during the fundraising journey. Investors evaluating a company for Series A often look closely at the reliability, scalability, and cost efficiency of its technology stack. GoCloud helps startups prepare for this stage by designing investor-ready cloud architectures, optimizing operational costs, and ensuring platforms can scale rapidly as the business grows. By strengthening the technical foundation of a startup and aligning infrastructure with long-term growth goals, GoCloud indirectly improves a company’s readiness for venture capital funding and makes it more attractive to institutional investors.

Frequently Asked Questions :

Q1: What is Series A funding?

Series A funding is the first major institutional venture capital round a startup raises, typically between $5M and $30M, in exchange for preferred stock. It follows seed funding and is used to scale a proven business model.

Q2: What is the Series A funding meaning in simple terms?

It’s the first time professional VC firms invest in your startup at scale. You’ve proven the product works (seed); now you’re raising capital to build the machine that sells and delivers it repeatedly.

Q3: What is a typical Series A valuation in 2025?

Based on Q4 2024 Carta data, the median pre-money valuation was approximately $45M — but this varies by sector, geography, and growth rate. Early-stage AI companies often command higher premiums.

Q4: What is Series A vs Seed funding?

Seed rounds are typically $500K–$3M from angels or micro-VCs to build an MVP and find initial customers. Series A is $5M–$30M from institutional VCs to scale a model that’s already working. The key difference is proof: seed bets on potential; Series A bets on demonstrated traction.

Q5: What is Series A vs Series B?

Series A builds the go-to-market engine. Series B scales it aggressively. Series B investors expect 2× or more revenue growth since Series A, a larger proven team, and a repeatable sales motion. Series B rounds typically range from $20M to $60M+.

Visual Guides to the Series A Journey :

Visual 1: Startup Funding Stages Timeline :

Visual 2: Series A Fundraising Flowchart :

Visual 3: Burn Rate + Runway — Before and After Series A :

Key Takeaways :

- Series A funding is the first institutional VC round, typically $5M–$30M in exchange for preferred stock at a pre-money valuation of $15M–$80M

- Series A vs Seed: Seed validates; Series A scales. Different investors, different proof bars, different governance implications

- What investors want: Product-market fit evidence, scalable unit economics (LTV:CAC ≥3:1), 6+ months of consistent growth, and a team that can execute

- The process has five stages: Prove traction → build narrative → target investors → diligence + term sheet → close + governance

- The most common mistakes are raising from the wrong investors, lacking a go-to-market story, underestimating capital needs, and entering the market with a weak cap table

- Start preparing 6–12 months early: Build your data room, clean your cap table, convert SAFEs, and build VC relationships before you formally raise

- Typical dilution is 15–25% — model your cap table before you negotiate, not after

Conclusion :

Understanding what Series A funding is — and, more importantly, when and how to raise it — is one of the highest-leverage skills a founder can develop. The difference between a founder who raises Series A at a strong valuation with aligned investors and one who either raises too early, too late, or with the wrong terms can define the entire trajectory of a company.

The framework is straightforward, even if execution is hard: build real traction, know your metrics cold, get warm introductions to the right investors, negotiate terms thoughtfully, and close with a data room that’s already built.

For startups building modern cloud-native infrastructure and scalable digital products, partners like GoCloud can play an important role by helping companies design reliable cloud architecture, optimize infrastructure costs, and prepare their platforms for rapid growth — a factor investors often look for when evaluating Series A-stage companies.