The best business loans for startups include SBA microloans (up to $50K, 8–13% APR), SBA 7(a) loans (up to $5M, lowest rates), online term loans (fast, flexible, higher cost), and business lines of credit (best for cash flow gaps). The right option depends on your credit score, time in business, revenue, and what the capital is for.

Step 1 — Evaluate Your Startup’s Funding Needs :

Evaluating your funding needs before applying is the single most important step.

Before you compare a single lender, get crystal-clear on three things: how much you need, what you need it for, and when you need to pay it back. Borrowing the wrong amount — or the wrong product — will either leave you undercapitalized or saddled with debt your cash flow can’t service.

Start by building a startup budget template and financial projections that answer:

- How much capital do you actually need? Add a 20–30% buffer for unexpected costs.

- What is the capital for? Each use case has an optimal loan product.

- How will you repay it? Lenders underwrite your DSCR (Debt Service Coverage Ratio) — the ratio of operating income to debt obligations. Most require a DSCR of at least 1.25×.

Working Capital vs Equipment vs Inventory vs Hiring :

Different funding needs call for different loan products:

| Use of Funds | Best Loan Product | Why |

| Cover operating expenses, gaps between receivables/payables | Business line of credit | Draw only what you need; pay interest on drawn balance only |

| Purchase machinery, vehicles, or technology | Equipment financing | The asset is collateral — no additional security needed |

| Stock inventory ahead of a demand spike | Short-term term loan or LOC | Predictable repayment tied to inventory cycle |

| Hire staff before revenue catches up | SBA microloan or revenue-based financing | Lower rates, mission-aligned for early-stage businesses |

| Acquire a business or purchase real estate | SBA 7(a) loan | Designed specifically for these use cases |

Mismatching use of funds to loan product is one of the most common — and costly — mistakes founders make.

Step 2 — Understand What Lenders Look For :

Most startup founders approach lenders with optimism about their idea and not enough data about their own risk profile. Lenders don’t fund ideas — they fund repayment probability. Know where you stand before you apply.

Credit Score Requirements :

Your personal credit score is the primary underwriting lever for startup loans, because most early-stage businesses don’t yet have a business credit history.

- 680–750+: Qualifies for SBA loans, bank LOCs, and competitive term loans at the best rates

- 640–679: Qualifies for online lenders and many fintech lenders; expect higher APR

- 600–639: Limited to alternative lenders, revenue-based financing, and some equipment lenders

- Below 600: Very limited options; consider microloans, Kiva (peer-to-peer, no credit check), or secured loans with strong collateral

Average business loan interest rates at traditional banks range from 6.3% to 11.5% APR — but borrowers with weaker credit profiles at online lenders often pay 25–50%+ APR.

Approval lever: Pull your personal credit report before applying. Dispute any errors — a single disputed item can shift your score 20–30 points.

Time-in-Business Benchmarks :

Time in business is the second-biggest underwriting gate. Here are the realistic minimums by lender type:

- Traditional banks / SBA loans: 2+ years in business (SBA technically allows less, but most partner banks want 2 years)

- Online/fintech lenders (OnDeck, Fundbox): 6–12 months

- Equipment financing: Often 0–6 months if the asset provides sufficient collateral

- SBA microloans (via nonprofit intermediaries): Startup-friendly — can qualify with 0–6 months

- Kiva: No minimum time in business

If you’re under 12 months old, traditional term loans and most bank products are largely off the table. Focus on microloans, equipment financing, or revenue-based options.

Document Requirements (Bank Statements, Plan, Projections)

Even fintech lenders that approve in minutes will pull these. Have them organized before you start any application:

- Last 3–6 months of business bank statements

- Business and personal tax returns (2 years if available)

- Profit & loss statement and balance sheet

- Business plan with executive summary

- Financial projections (12–24 months) — see our startup financial projections guide

- Government-issued ID + Social Security Number

- Articles of incorporation or business license

- Any existing loan or lease agreements

Best Business Loan Types for Startups :

The right loan mix depends on your stage, revenue, and capital use.

Online Term Loans (Best for Predictable Repayment)

Online term loans provide a lump sum of capital repaid over a fixed schedule — monthly or weekly — at a fixed or variable interest rate. They’re the workhorse product for startups that need a defined amount of capital for a specific purpose.

Best for: Hiring, marketing campaigns, product development, or any use with a predictable ROI timeline.

- Lenders: OnDeck ($5K–$400K, terms up to 24 months, same-day funding available), Funding Circle (competitive rates, longer terms)

- Typical APR: 15%–50% (online lenders); 6–11% (bank lenders)

- Min requirements: 6–12 months in business, 600+ credit score, $50K+ annual revenue

- Watch out for: Origination fees (1–5% of loan amount), prepayment penalties, and daily/weekly repayment schedules that hammer cash flow

Business Lines of Credit (Best for Cash Flow Gaps)

A business line of credit (LOC) is revolving capital you draw from as needed — you only pay interest on what you actually use. It’s the most flexible form of debt financing for early-stage businesses.

Best for: Managing seasonal cash flow gaps, bridging receivables delays, or covering unpredictable operating expenses.

- Typical amounts: $10K–$250K

- Typical APR: Prime + 1.75% (secured, bank) to 20–40% (unsecured, fintech)

- Min requirements: 6 months in business, 600+ credit score, $20K–$50K in monthly revenue

- Lender examples: Fundbox (up to $250K, 600 min FICO, 3-minute approvals), Credibly, Wells Fargo BusinessLine

The key trade-off: secured LOCs require collateral but offer far lower rates; unsecured LOCs are faster but carry significantly higher APRs and often require a personal guarantee.

SBA Loans for Startups (Best Rates, Hardest to Qualify)

U.S. Small Business Administration (SBA) loans are government-backed loans originated by private lenders. The SBA guarantees a portion of the loan (up to 85%), which reduces lender risk and results in capped rates — making them the cheapest institutional debt available to small businesses. Use the SBA Lender Match tool to find a participating lender near you.

SBA 7(a) Loans :

The SBA’s flagship program. Available for almost any business purpose: working capital, real estate, equipment, acquisitions, and more.

- Max loan amount: $5 million

- SBA guarantee: 85% (loans ≤$150K); 75% (loans >$150K)

- Interest rates: Capped at base rate + 3.0% to 6.5%, depending on loan size. With the current prime rate at 6.75%, effective rates range from approximately 9.75% to 13.25% for smaller loans

- Best for: Startups with 2+ years of history, strong personal credit (680+), and a clear repayment source

- Key requirement: Must be unable to obtain credit on reasonable terms elsewhere; must meet SBA size standards

SBA Microloans :

SBA microloans are the most founder-friendly government loan program for early-stage businesses — and the most overlooked.

- Max loan amount: $50,000 (average is ~$13,000)

- Interest rates: 8%–13%, set by the nonprofit intermediary lender

- Repayment terms: Up to 7 years

- Eligible uses: Working capital, inventory, supplies, furniture, fixtures, machinery, equipment — cannot be used to pay existing debt or purchase real estate

- Who qualifies: Startups at any stage; requirements are set by individual intermediary lenders (nonprofits), not banks

- Key advantage: Many microloan intermediaries provide free business training and technical assistance alongside capital — especially valuable for first-time founders

If you’re under 12 months old with limited revenue, the SBA microloan program is often the single best first loan to pursue.

Equipment Financing (Best When You Have Assets)

Equipment financing lets startups purchase machinery, vehicles, technology, or any capital asset — and the equipment itself serves as collateral. This structure means lenders can approve startups that wouldn’t qualify for unsecured term loans.

- Typical amounts: $5K–$500K+

- Typical APR: 4%–11% (secured by asset)

- Down payment: 0%–20% depending on lender and creditworthiness

- Min credit score: 510–650 (lender-dependent)

- Time in business: Often 0–6 months if the asset covers the loan value

- Best for: Restaurants buying kitchen equipment, manufacturers buying machinery, logistics startups buying vehicles

The borrower-friendly element: because the asset is collateral, equipment financing is one of the few products where a brand-new startup can qualify with relatively weak financials.

Invoice Financing / Factoring (Best for B2B Receivables)

If your startup sells to other businesses (B2B) and issues invoices with net-30 to net-90 terms, you’re essentially extending interest-free loans to your customers while your own cash flow suffers. Invoice financing solves that.

- How it works: You sell outstanding invoices to a factoring company for 80–90% of their face value, upfront. The factor collects directly from your customer, then remits the remaining balance minus a fee.

- Cost: Typically 1%–5% of invoice value per 30-day period

- Best for: Startups with strong B2B customers but slow-paying receivables; particularly common in construction, staffing, logistics, and professional services

- Key risk: Your customers know a third party is collecting. Some clients react negatively — vet your customer relationships before factoring.

Merchant Cash Advances (Fastest, Usually Most Expensive)

A merchant cash advance (MCA) is not technically a loan — it’s a purchase of future receivables. A lender advances a lump sum, repaid via a fixed percentage of your daily or weekly card sales, at a factor rate (typically 1.1× to 1.5×).

- Effective APR equivalent: Often 35%–150%+

- Speed: Same-day to 48-hour funding

- Best for: Retail and restaurant startups with consistent card volume facing a short-term cash crunch

- Bottom line: MCAs should be a last resort. The effective cost is dramatically higher than any other product listed here. Use only if you have exhausted every other option and have a clear repayment path.

Startup Business Loans With No Revenue :

The hard truth: most lenders require at least $50K–$100K in annual revenue. But several paths exist for pre-revenue or very early-stage founders.

Personal Credit-Based Options (Risks + Safeguards)

- Personal loans used for business: Available up to $50K–$100K at 7%–25% APR depending on credit score. Fast, accessible. Risk: If the business fails, your personal credit is destroyed and you’re liable for the full amount.

- Business credit cards with a personal guarantee: 0% intro APR periods (12–21 months) can function as interest-free working capital. Risk: Revert to 20–28% variable APR after the intro period.

- Safeguard: Never deploy personal credit into a business without 12+ months of projected runway. Model the repayment scenario if revenue takes 6 months longer than expected.

Collateral-Backed Options :

- Equipment financing with strong collateral: If you need capital to buy equipment, the asset covers the lender’s risk regardless of your revenue history.

- HELOC or home equity loan: Founders with real estate equity sometimes leverage it for startup capital. Effective, but puts personal property at risk — use only when other options are exhausted.

- SBA microloans: Intermediary lenders set their own requirements; many will lend to pre-revenue founders with collateral, a strong plan, and personal guarantee.

Comparison Table: Startup Loan Options Side-by-Side :

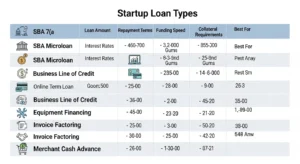

| Loan Type | Best For | Typical Speed | Typical Cost (APR) | Key Requirement | Main Risk |

| SBA 7(a) | Working capital, real estate, acquisitions | 2–3 months | ~9.75%–13.25% | 2+ yrs in business, 680+ credit | Slow; requires strong financials |

| SBA Microloan | Early-stage, small capital needs | 2–4 weeks | 8%–13% | Varies by intermediary | Low amounts ($50K max) |

| Online Term Loan | Defined capital for a specific purpose | 24–72 hours | 15%–50% | 6–12 months, 600+ credit | High APR; weekly payments |

| Business LOC | Cash flow gaps, revolving needs | 24 hours–1 week | 10%–40% | 6 months, $20K/mo revenue | Can over-draw; variable rate |

| Equipment Financing | Purchasing capital assets | 1–5 days | 4%–11% | Asset as collateral | Asset repossession on default |

| Invoice Factoring | B2B receivables, slow-paying clients | 24–48 hours | 12%–60% effective | Outstanding B2B invoices | Customer relationship risk |

| Merchant Cash Advance | Immediate cash, consistent card sales | Same day | 35%–150%+ effective | Daily card volume | Extremely high cost |

What You Need to Apply :

Step 1: Check your personal credit score and pull your credit report. Dispute any errors before applying.

Step 2: Determine your loan amount and primary use of funds. Match the use case to the right product (see Step 1 of this guide).

Step 3: Gather all required documentation (see Table 2 below).

Step 4: Research lenders that match your profile. Use the SBA Lender Match tool for SBA options; compare at least 3–5 lenders for non-SBA products.

Step 5: Submit applications in a focused window. Multiple hard credit inquiries within a 14–45 day window typically count as one inquiry for scoring purposes.

Step 6: Review all terms before signing. Scrutinize the APR (not just the rate), origination fee, prepayment penalty, and any personal guarantee clause.

Table 2: Application Checklist :

| Document | Why It Matters | Pro Tip |

| Last 3–6 months of bank statements | Primary cash flow verification | Ensure no overdrafts in the 90 days prior to applying |

| Business and personal tax returns (2 years) | Verifies income and tax compliance | File on time — delinquent filings are automatic rejections at most lenders |

| Profit & loss statement | Shows revenue trend and margins | Have a CPA-prepared or CPA-reviewed version for SBA applications |

| Financial projections (12–24 months) | Demonstrates repayment capacity | Tie projections to real assumptions — lenders interrogate the inputs |

| Business plan | Contextualizes use of funds | Lead with the executive summary; keep total length under 15 pages |

| Cap table (if applicable) | Shows ownership structure | Clean up any undocumented equity before applying |

| Articles of incorporation + business license | Confirms legal standing | Ensure your entity is in good standing in your state of registration |

| Accounts receivable aging (if applicable) | Required for invoice financing | Shows quality and aging of outstanding invoices |

| Collateral documentation | Secures the loan; reduces lender risk | Have appraisals or purchase records ready for real estate and equipment |

Business Plan + Projections :

Lenders are not evaluating your business plan for its vision — they’re using it to answer one question: “Will this business generate enough cash flow to service this debt?” Your projections should show a conservative base case where DSCR stays above 1.25× even if revenue comes in 20% below target.

Collateral + Guarantees (What They Mean)

A personal guarantee means you are personally liable for the loan if your business defaults — your personal assets (home, savings, investments) can be seized. Almost all SBA loans and most startup loans require one.

Collateral is a specific asset pledged to secure the loan. If you default, the lender can seize and liquidate it. Common collateral types:

- Real estate (most favorable to lenders)

- Equipment or vehicles

- Accounts receivable / inventory

- Cash deposits or CDs

An unsecured loan with no collateral will almost always carry a higher APR and require a stronger credit profile. The more collateral you can offer, the lower your rate.

What to Do If You Get Rejected :

Rejection is data, not defeat. Here are the fixes ranked by typical impact :

- Find out exactly why you were declined. Lenders are required to give you an adverse action notice. This tells you whether rejection was credit-based, revenue-based, or documentation-based — each requires a different fix.

- Fix your credit (highest impact for credit-based rejections).

- Dispute errors on your credit report — even one incorrect derogatory item can cost you 30+ points

- Pay down revolving balances below 30% utilization

- Avoid new hard inquiries for 60–90 days

- Build 3–6 more months of banking history. Many fintech lenders use bank statement underwriting. More months of clean, growing deposits directly moves the approval needle.

- Apply to a different loan type. A rejection from a bank term loan doesn’t mean you’re rejected from an SBA microloan, equipment financing, or revenue-based financing. Each product has different underwriting logic.

- Reduce the loan amount. A smaller ask at a lower LTV (loan-to-value) or with stronger collateral coverage materially improves approval odds.

- Bring in a co-signer or guarantor. A creditworthy co-signer with personal assets can unlock options unavailable to the borrower alone.

- Work with a CDFI (Community Development Financial Institution). Organizations like Accion Opportunity Fund specifically serve startups and founders who don’t qualify at traditional lenders — often at competitive rates.

Alternatives to Startup Business Loans :

Debt is not always the right tool. Before borrowing, consider whether non-dilutive or equity-based capital better fits your stage and risk profile.

Business Credit Cards :

A 0% intro APR business card can function as 12–21 months of interest-free working capital — essentially free debt if you pay the balance before the intro period expires. Best for: marketing spend, software subscriptions, and inventory with a short cash cycle. Worst for: large capital expenditures you can’t repay within the intro period.

Grants (Brief)

Small business grants don’t require repayment or equity. Highly competitive but genuinely free capital. Federal, state, and private grant programs exist for minority-owned businesses, veterans, women founders, rural businesses, and specific industries (deep tech, climate, healthcare).

Crowdfunding (Brief)

Reward-based crowdfunding (Kickstarter, Indiegogo) and equity crowdfunding (Regulation CF) let you raise capital directly from customers and the public — without a bank. Best for: consumer product startups with compelling narratives and built-in audience.

Angel / VC Investment (Brief)

If your startup has high-growth potential, equity capital from angel investors or venture capitalists may be more appropriate than debt. You’re not borrowing — you’re selling ownership. No repayment obligations, but you give up equity and control.

How GoCloud Supports Startups in Managing Business Loan Funding :

Securing a business loan is only the first step for many startups — the real challenge is using that capital efficiently to build scalable systems and sustainable growth. This is where GoCloud can play a valuable role. By helping startups design reliable cloud infrastructure, optimize hosting costs, and implement scalable digital architectures, GoCloud ensures that borrowed capital is invested in technology that supports long-term growth. When startups use loan funding to build digital platforms, SaaS products, or online services, a well-planned cloud strategy reduces operational waste and improves performance. As a result, founders can deploy their loan capital more effectively, maintain healthier cash flow, and scale their business with greater confidence.

FAQs :

Q1: What is the easiest startup business loan to get?

SBA microloans and online lenders like Kiva (peer-to-peer, no interest, no credit check) are the most accessible for very early-stage startups. Fundbox and OnDeck have relatively low bars for online term loans and credit lines with 6 months of business history.

Q2: Can I get a business loan with no revenue?

Yes, but options are limited. SBA microloans (via nonprofit intermediaries), equipment financing (when asset serves as collateral), and personal credit-based products are your most realistic paths. Peer-to-peer lenders like Kiva don’t check revenue at all.

Q3: What credit score is needed for a startup business loan?

Most online lenders require a minimum personal credit score of 600. SBA loans and bank term loans typically want 680+. Equipment financing can go as low as 510 with sufficient collateral. Better credit means lower rates — the gap between a 620 and 720 score can mean 10–20+ percentage points in APR.

Q4: How much can a startup borrow?

Amounts range from $500 (Kiva) to $5 million (SBA 7(a)), depending on the product, your revenue, creditworthiness, and collateral. Most first-time startup borrowers realistically access $10K–$150K through online lenders or microloans.

Q5: What is the interest rate on startup business loans?

Interest rates for startup business loans range from 8%–13% (SBA microloans) to 35%–150%+ (merchant cash advances). Bank and SBA rates run 6.3%–13.25%. Online fintech lenders typically charge 15%–50% APR. Always compare APR — not just the monthly payment or factor rate.

Conclusion :

The best business loan for your startup is the one you can actually qualify for, afford to repay, and that matches your specific capital need. There’s no universal “best” product — there’s only the right product for your stage, your credit profile, and your use case.

For startups building digital platforms or scaling online services, working with a reliable cloud partner like GoCloud can also help optimize infrastructure costs and ensure your technology stack is ready for growth, making it easier to manage funding efficiently as your business expands.